Investment Thesis

A regulated monopoly with predictable cash flow. TNB owns the National Grid, and its return are locked in under the IBR framework

Key beneficiary of Malaysia’s data centre and energy transition boom. Record capex in RP4 expand its asset base that will translate into higher returns.

Dividend stock with growth potential. With improved fuel cost adjustments under RP4, dividend visibility and upside look stronger going forward.

⚠️Disclaimer: Word of Caution!

Please DO NOT take this educational post as a buy or sell signal. When it comes to investing, it is important to have your own judgement. Despite my detailed analysis, mistakes may occur, and blindly following could lead you to make similar errors and financial losses. Furthermore, I AM NOT a licensed financial advisor. I’m merely sharing my experiences and opinions only.

Additionally, please note that I hold positions in the discussed stock, and my view may be biased as a result.

In my previous post, I’ve shared in-depth about Malaysia’s energy landscape. If you haven’t read about it, you can read it here. In this post, I want to talk about Tenaga National Berhad (TNB) and why I think this company is a good dividend-paying stock.

🏢Type of Company

TNB is a utility company. It sits indirectly within the AI value chain because AI runs on data that is stored and processed in Data Centres (DC) which are extremely power-hungry. This means rising data centre activity in Malaysia should translate into higher electricity consumption. As such, I see TNB as a key beneficiary of the local DC boom.

Additionally, the company is also a dividend-paying stock. It has a dividend policy to distribute 30% to 60% of its adjusted PATAMI. Since 2018, it has been paying out dividend consistently at above 50%. This is despite the fact that there is a pandemic in 2020. Below is TNB’s historical dividend per share in cents (excluding special dividend) from 2014 to 2024:

Based on the above, this is a “Category 2” type of dividend paying company as described in my book. It pays a constant dividend that doesn’t increase yearly over past 10 years – it is not a straight line up.

However, I think this will change soon. I will explain more in the growth catalyst section.

💡Business Model

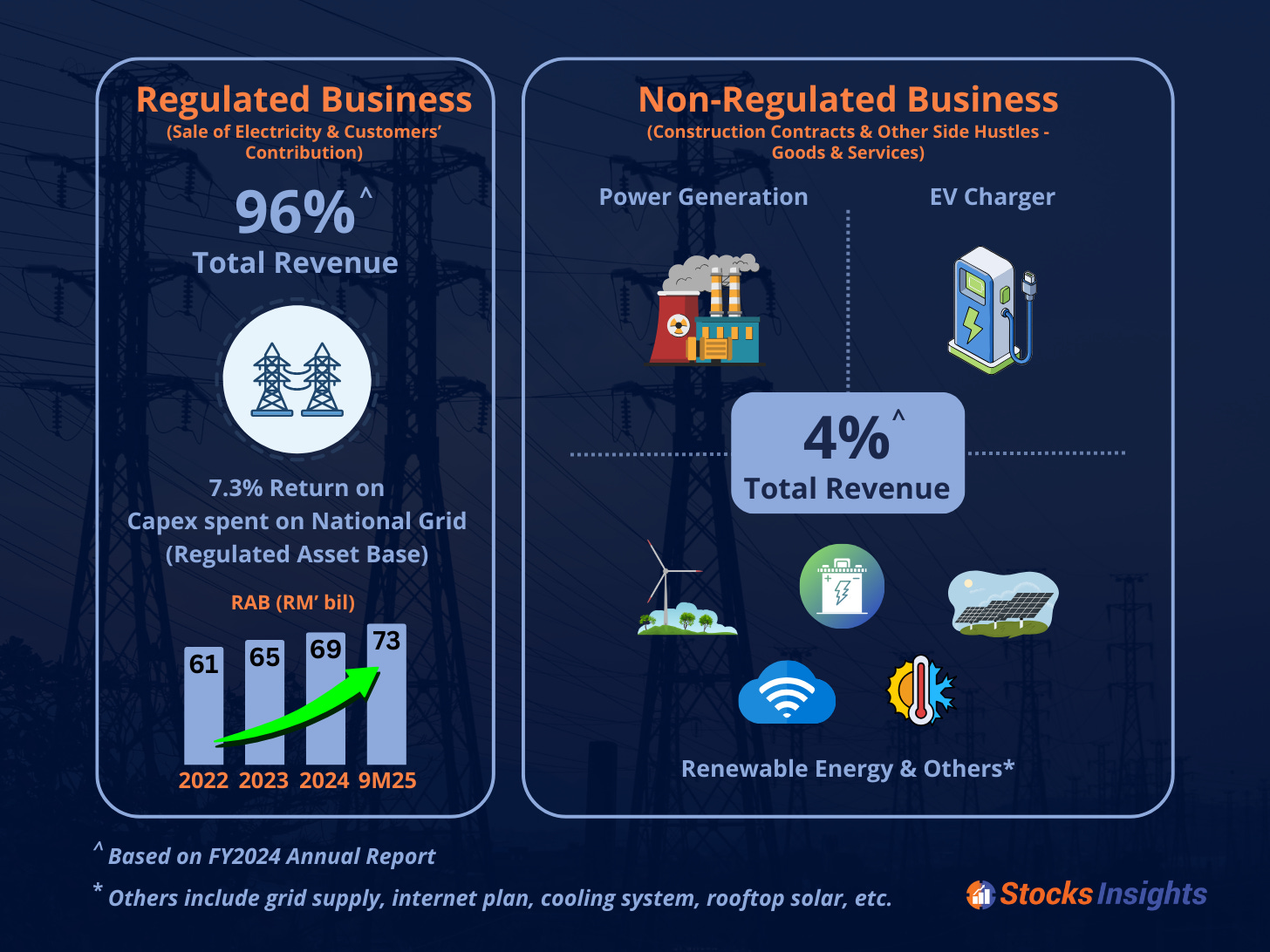

TNB makes money through several different “buckets”. One part of their revenue is regulated by EC (remember the ARR?) and the other part is unregulated. The company also has businesses overseas which are mainly related to renewable energy. However, it only accounts for 4% of total revenue in 2024 - not worth looking into it in detail.

Here’s an overview with revenue breakdown as of 2024:

⚡️Bucket #1: Sale of Electricity (The “Monthly Bill”)

This is the monthly electricity bill to consumers at a specified tariff rates based on the IBR framework. In 2024, about 96% of TNB’s total revenue came from electricity sales.

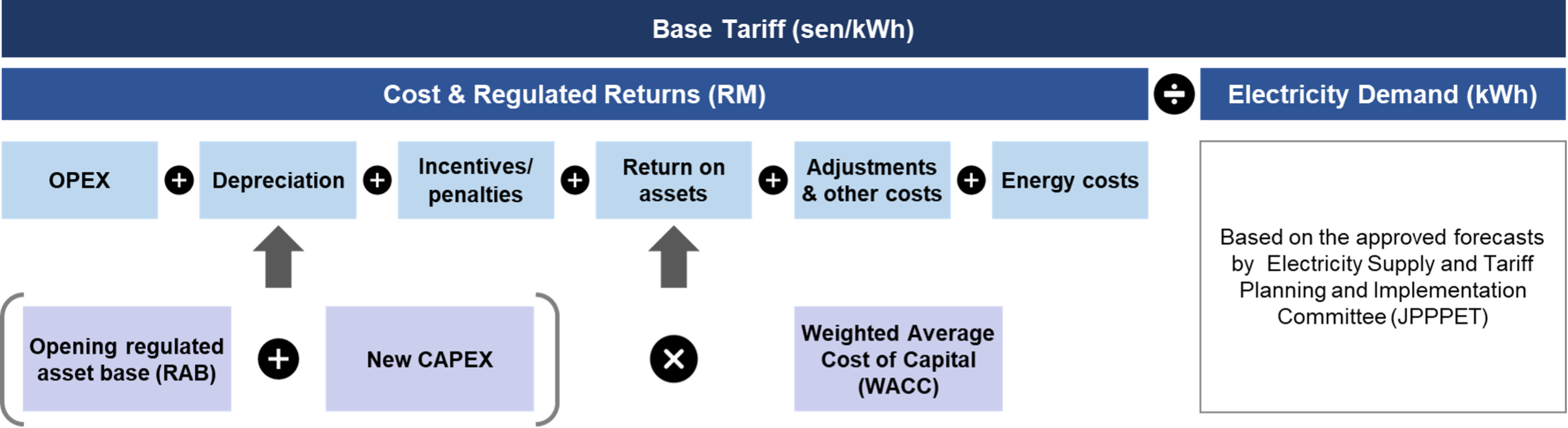

The formula for this tariff rate is as follows:

The base tariff is the rate that TNB use to bill the consumers. Note that not all of revenue collected ends up in TNB’s pocket.

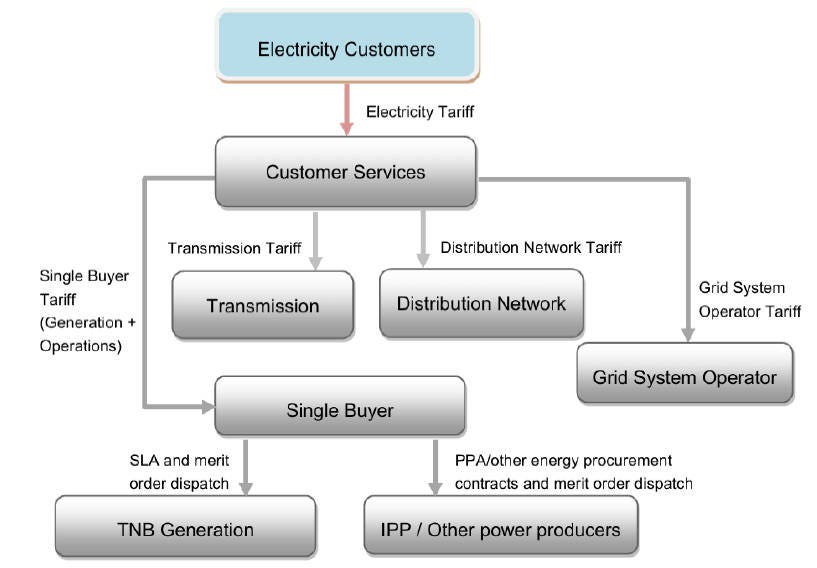

A large portion of this revenue aim to recover the operating costs as depicted in the above formula. These are costs incurred by other regulated functions such as Single Buyer (SB) and Grid System Operator (GSO).

TNB’s true earnings as per the formula above is dependent on below 3 components:

Regulated Asset Base (RAB) which is the National Grid asset value

New CAPEX for power grid upgrades & maintenance

Allowed rate of return which is the WACC

In a nutshell, TNB’s profit is not based on how much electricity consumers use. Instead, it is on how much it spent in upgrading & maintenance of the National Grid.

The bigger the spending (capital), the higher the RAB. This then translates into higher returns for TNB. I will explain more in the growth catalyst section later.

This bucket also includes an unregulated business which is the power generation sale to SB. As explained in previous post, the revenue from this business is dictated in the service agreement between TNB and the SB.

👨🔧Bucket #2: Construction of Electrical Systems

Sometimes, TNB is hired to build power-related infrastructure for other companies or the government, like setting up a new substation or moving giant power lines for a new highway.

This is a competitive business where TNB bids for work just like any other construction company. In 2024, this bucket of business only contributes 0.2% of total revenue.

🔌Bucket #3: Customers’ Contribution (“The connection fee”)

Whenever a developer builds a new building such as shopping mall, housing estate or data centers, they have to pay TNB to connect that new area to the main power grid.

In 2024, this bucket of business only contributes 0.5% of total revenue.

🔋Bucket #4: Other Side Hustles (Goods & Services)

This is a mix of smaller unregulated businesses which includes EV charging, rooftop solar installation, fiber-optic internet (Allo), consulting, and maintenance work that are related to electrical infrastructure.

🛡️Moat: Government Regulation

In my book, I listed out 4 common types of economic moats that Malaysian companies can have. Based on TNB’s business model described above, its competitive advantage is government regulation.

As mentioned in previous post, TNB owns 100% of the national power grid in Peninsular Malaysia. It is illegal for anyone else to build a competing power grid. This effectively gives TNB a natural monopoly position in transmission and distribution segments.

However, this does not mean TNB can raise prices freely. Tariffs are still governed by the IBR framework:

When revenue falls short due to weaker demand, regulators can adjust tariffs to recover the allowed revenue;

When revenue exceeds the allowed level, the excess is returned to consumers via rebates or lower tariffs.

The upside of this IBR framework is TNB will have very stable and predictable earnings. This is evidenced by their resilient earnings during pandemic period in 2020 despite lower power demand.

🌱Growth Catalyst

The main growth driver for TNB is the expansion of its RAB. As explained earlier, TNB’s true profit drivers are essentially:

(RAB + New CAPEX) x WACC

Under the latest IBR framework (Regulatory Period 4 or RP 4), TNB is permitted to spent RM42.82 bn over 3 years from 2025 to 2027 and earn a regulated return of around 7.3% on its invested capital.

However, not all RM42.82 bn can be spent fully. This approved CAPEX is split into:

Base CAPEX (RM26.55 bn): For routine power grid upgrades and maintenance purposes.

Contingent CAPEX (RM16.27 bn): This is driven by specific conditions such as unexpected surge in electricity demand from data centers that require expansion of power grid or battery energy storage systems (BESS).

CIMB analyst is expecting TNB to spend 60% to 70% of the contingent CAPEX in RP4. Based on this, it’s safe to say that TNB’s RAB will expand by at least RM36 bn.

Below is the company’s historical RAB from 2015 to 9M25 which is growing steadily at 4.3% CAGR:

In the past from RP 1 to RP 3, the approved CAPEX has always been hovering between RM18 bn to RM21 bn. The latest RP 4 has doubled this CAPEX amount and I believe it was mainly driven by 2 reasons:

💾Surge in Data Center (DC) investments

Since Singapore’s 2019 moratorium on new DC projects due to land constraints and massive strain on its power grid, Malaysia has experienced a surge in DC projects. The National Grid needs to be upgraded to support DC’s demand of high-voltage and ultra-stable connections.

In TNB’s 3Q25 Analyst Briefing, it highlighted that the electricity demand grew 5.2% yoy from DC. To-date, the company has secured 49 DC projects in the pipeline. This means more power consumption is coming.

🎯National Energy Transition Roadmap (NETR)

This framework, launched in 2023, outlines a roadmap to accelerate Malaysia’s shift from fossil fuel-dependent economy to a high value, low-carbon one. The ultimate goal of this NETR is to achieve Net-Zero greenhouse gas emissions by as early as 2050.

For TNB, it serves as a justification for government to increase TNB’s CAPEX to modernize the National Power Grid infrastructure. You cannot just plug a solar farm into an old grid. The system needs to be smarter to handle intermittent power.

According to CIMB analyst, 64% of the total contingent capex (RM16.3 bn) will be allocated to facilitate energy transition roadmap by TNB.

📈Likelihood of Higher Dividend Payment

As explained earlier, TNB has a target dividend payout of 30% to 60% of its adjusted Profit After Tax and Minority Interests (PATAMI).

In 2024, the company already pays DPS of RM0.51. Question is, can it still increase further for year 2025 & beyond?

I think it is very likely because of below reasons:

Higher approved CAPEX which will drive TNB’s RAB higher as explained in growth catalyst section above

Stable cash flows due to the implementation of automatic fuel adjustment (AFA) mechanism which automatically adjust fuel price fluctuations on monthly instead of every 6 months. Additionally, TNB’s reported PATAMI will be more accurate in reflecting its core regulated business.