Summary

An epic market overreaction. A ~35% AI-driven sell-off ignores strong double-digit RPO growth, proving enterprise software demand remains highly resilient.

“Systems of record” are the ultimate moat. Foundational data platforms and cybersecurity remain indispensable, as AI agents rely entirely on their proprietary data and strict guardrails.

A rare margin of safety. The current valuation compression offers a prime opportunity to accumulate high-quality enterprise SaaS while avoiding vulnerable creative software.

⚠️Disclaimer: Word of Caution!

Please DO NOT take this educational post as a buy or sell signal. When it comes to investing, it is important to have your own judgement. Despite my detailed analysis, mistakes may occur, and blindly following could lead you to make similar errors and financial losses. Furthermore, I AM NOT a licensed financial advisor. I’m merely sharing my experiences and opinions only.

Additionally, please note that I hold positions in the discussed stock, and my view may be biased as a result.

Recently, there has been a crash in US software companies. My holdings in software stocks such as MSFT, PANW, SNOW, NOW, FDS, and SNPS are all showing negative returns this year.

When I look at the software sector ETF (IGV), which I use as a proxy for the broader software market, it is down ~35% since October 2025. This firmly places the sector in bear market territory:

The market dubbed this "SaaSpocalypse". As a long-term investor, the last thing I want to do is “panic”. Instead, I should find answers to 2 critical questions:

What triggered this sell-off?

Is this a permanent fundamental deterioration or a market over-reaction?

#1: What Triggers The Sell-Off?

Here’s the timeline of the sell off:

Mid-Oct 2025: Sector Rotation

After the massive bull run from the 2022 bear market lows, tech stock as a whole (including software) were trading at historically stretched forward PE multiples. The market seems to think it has become bubble. As such, many started to rotate out of tech stock.

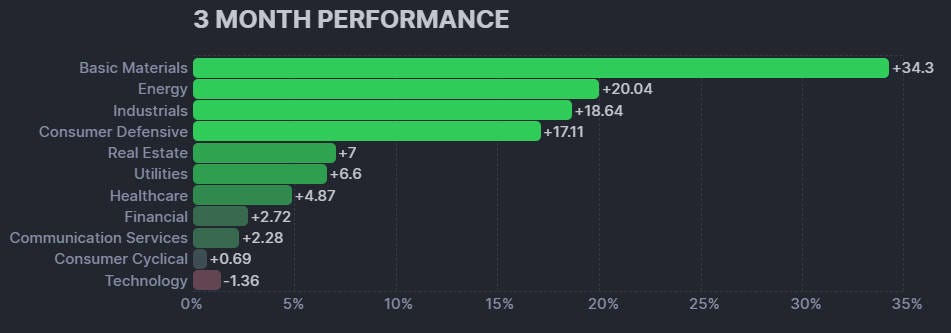

Below is S&P 500 Index 3-months performance to time time of writing this post:

Sector such as basic materials, energy, industrials and consumer defensive were all being favored by the market. In my opinion, it was a healthy pullback but it was not big enough.

Late-Jan 2026: AI Capex & ROI Fears

As Q4 2025 earnings rolled in, the market suffered severe sticker shock. Alphabet, Amazon, Meta, and Microsoft revealed intentions to spend a combined $680 bn on AI Infrastructure in 2026, a staggering 70% increase from estimates in 2025.

Alphabet: Guided about $175 - $185 bn capex in 2026. This is nearly doubled the amount in 2025.

Amazon: Guided about $200 bn capex in 2026, 53% increase from last year.

Meta: Expect $115-$135 bn capex in 2026. This is also nearly double from last year level.

MSFT: Expect to spend $75 bn capex in first half of 2026. The annualized amount points to a $140 bn.

Tesla: Expect capex for 2026 to exceed $20 bn, up significantly from $8.5 bn last year.

Apple: Expect to spend around $13 bn, which is similar to last year. They are the only outlier but not surprising since they leverage of others to power its Apple Intelligence features.

This spending spree has led to negative impact on companies’ free cash flows (FCF). In the past, the market likes these tech stocks because they are asset light that can generate steady FCF. In turn, these FCF is use to buyback shares.

This narrative seems to have changed. Many of the Mag 7 is now taking on debt to further fund their AI Infrastructure spending. The realization that monetizing AI takes longer than anticipated have caused the market to sell-off aggressively.

3rd Feb 2026: Agentic AI Disruption (The Knockout Blow)

The third trigger point is when Anthropic released new plug-ins for its Claude “Cowork” agent. These plug-ins are tailored for Legal, Sales, Marketing and Financial analysis. When integrated with legacy systems, the plugin can autonomously perform actions as told.

This rattled the market because if AI agents can do more work with fewer people, traditional software that charges per user (or “per seat” basis) may see demand growth slow or worse - a reduction in revenue. It erodes the core business models of legacy SaaS companies, data providers, and workflow tools.

IGV dropped another 11% over the next 3 days to 5th Feb. At the time of writing, the ETF has been consolidating within range $76.3 and $86.1.

Late-Feb 2026: The Cybersecurity Shock…

As if this was not enough, Anthropic launched “Claude Code Security”. It is an enterprise-focused AI capability built into the Claude Code platform that scans entire codebases for security vulnerabilities and automatically suggests targeted software patches to fix them.

Traditional cybersecurity tools rely heavily on rigid rules and matching code against databases of known vulnerability signatures. In contrast, Claude Code Security reads and reasons through code contextually, allowing it to identify complex "Zero-Day" vulnerabilities, such as flaws in business logic or broken access control, that traditional methods often miss.

Consequently, this triggered a violent sell-off on big cybersecurity stocks like Crowdstrike (-19%), Zscaler (-17.2%), Okta (-16.8%), Palo Alto (-10.4%), etc.

#2: Over-reaction or Structural Problems?

To understand whether the software sell-down are justified or not, one must understand how Claude AI works.

How Claude AI Works?

When analysts say “AI agents will disrupt software,” they are often vague and lack details as to how. What has actually changed is that Claude can now connect to a company’s systems and execute repeatable workflows autonomously using two key features:

⛓️💥MCP: the “USB port” for enterprise data

Claude’s Model Context Protocol (MCP) provides a standardized way for its AI model to connect to company’s systems (e.g. databases, file drives or internal tools). Just like a “USB port” where any operating system can access the file as long as a compatible USB drive is connected to this USB port.

This MCP reduces the need for custom built application programming interface (APIs) to integrate between two or more systems.

📜Skills: packaged “SOPs” (Standard Operating Procedures)

Claude’s “Skills” are lightweight, reusable workflow packages. They teach the AI how to do a specific job without requiring a long, complex prompt every time.

If MCP provides access to the kitchen & tools, "Skills" are the step-by-step recipes that teach AI how to use those tools effectively.

Anthropic has pre-built some skills (e.g. creating docs, presentation slides, extract data from PDFs or spreadsheets, etc.) and allows developers to create custom ones, potentially creating a marketplace similar to Apple's App Store.

🤖Synergy: MCP + Skills = An Autonomous Worker

Combined, they create a digital employee because:

Skill defines the workflow (“what good looks like”, risk rules, output format, etc.).

MCP pulls data and pushes actions into systems (databases, CRM, document storage, etc.) as required by the Skills.

AI isn’t just answering questions. It now can retrieve, decide and execute an action requested by the user.

How Does This Disrupt Software Companies?

For decades, software like Salesforce, ServiceNow or Snowflake monetize 2 big things:

Integration between systems (custom APIs)

Per-seats (per-user pricing)

Claude AI pressures both:

🔀Reduction of Middleware

In the past, if an ERP system like Oracle JDE needs to talk to HR management system like Workday, one must hire consultants or buy middleware. It is expensive because these require custom built for every system.

This type of integration are hardcoded meaning there is a defined workflow:

“When event A happens in Salesforce > call API B in NetSuite > map fields > write to table C”

Any changes in rules will need to rebuild the whole integration logic.

With the MCP, the AI can now connect to multiple systems via a standard interface and complete the workflow end-to-end autonomously.

User just need to specify an objective, example:

“Generate a renewal risk report and create tasks for the account team”

The AI decides:

which tools (Skills) to call,

what data sources to query via the MCP,

how to transform/ validate data,

and what actions to execute

This is known as “dynamic orchestration” because the path can change depending on what the AI agent finds. It compresses the value of middleware.

📉Reduced Demand for Seat-based SaaS

Because AI agent is now able to access company’s system of records and perform actions autonomously, companies now require less employees to perform certain tasks.

Here’s an example:

With the use of MCP & dedicated “sales skills”, company can deploy AI agent that autonomously carries below tasks:

Draft personalized marketing emails based on customer’s past sales transactions.

During deal negotiation stage, it able to connect into company’s sales database & update the deal stage, logs the summary and flags follow-up actions in real-time.

Traditionally, these tasks are done manually by employees.

As companies downsize, the “per-seat” pricing model used by SaaS giants like Salesforce may face significant revenue compression.

But…How True Are These? 🤔

Reading about these disruption rationale by various analysts seems to make logical sense. However… looking at the recent earnings of these SaaS companies tells a different story:

ServiceNow reported its Q4 2025 subscription revenue, growing 21% yoy. Its remaining performance obligation (RPO) is at $12.85 bn, up 25% yoy.

Salesforce reported its Q4 2026 subscription revenue, growing 13% yoy. Its RPO is at $72.4 bn, up 14% yoy.

Adobe reported its Q1 2026 subscription revenue, growing 13% yoy. Its RPO is at $22.2 bn, up 12% yoy.

Factset reported its Q1 2026 revenue, growing 6.9% yoy. Its annual subscription value grew to $2.4 bn, up 5.9% yoy.

Snowflake reported its Q4 2026 revenue, growing 30% yoy. Its RPO is at $9.77bn, up 42% yoy. Additionally, there’s 740 net new customer additions representing 40% yoy growth.

All of these companies are experiencing revenue growth rather than declining as alleged above. More importantly, their RPO — the total value of all signed service contracts yet to be delivered — is still growing.

My Verdict: Over-reactions 😱

The current sell-down is clearly a result of the market being panic. Market tends to sell first and ask question later. A nice way of describing this is “The market is a forward-looking mechanism”. Investors are not selling because of companies’ recent earning results.

They are selling because they believe AI agents will take over white-collar tasks and companies will refuse to renew thousands of software licenses over the next 3 to 5 years.

🔴Misconception of AI

However, I think people tend to forget below key concepts of AI and AI agent:

🎲AI is a probabilistic model. It does not guarantee 100% accuracy. Instead, it generates responses by determining which answer is statistically most likely to satisfy the user's intent.

🗃️AI agents require context to function effectively. This context is pulled from “systems of record” or “internal databases”; without this grounding, the agent cannot execute meaningful workflows.

Because of the above, AI can make mistake and also hallucinate. Example:

Claude AI “Skills” feature attempt to make the AI more deterministic by providing a step-by-step instructions to AI agents. However, this is still at the early stage.

According to a survey done by Prosper Insights & Analytics, most consumers are not yet comfortable with fully autonomous AI agent, especially in high stakes or emotionally sensitive scenarios.

It further stated that “AI cannot deliver consistent performance without human oversight, transparent governance, and clearly defined guardrails”. In other words, AI agent’s work requires human oversight.

I believe AI agent will change workers’ job role from “doer” to “reviewer”.

🔴SaaS Companies Are Evolving Too…

Additionally, SaaS companies are not sitting still. They have been actively defending their moats since 2023:

Salesforce (Late 2024): Launched Agentforce and Data Cloud, embedding native AI into the CRM for superior, real-time data context that external agents lack.

ServiceNow (Late 2023): Deployed “Now Assist” natively within its CMDB, enforcing strict access controls and data privacy that third-party agents cannot guarantee.

Adobe (Late 2023): Released Firefly, trained solely on licensed content, providing enterprise clients with critical legal indemnification against copyright risks.

FactSet (2023–2024): Embedded proprietary financial data directly into enterprise data warehouses, ensuring it remains the mandatory “ground truth” for any AI modeling.

Snowflake (Mid-2024): Launched Cortex AI, allowing clients to run LLMs securely inside their own data perimeter, eliminating the risk of data egress to external agents.

That said, I think AI will deeply penetrate creative sector precisely because art is inherently subjective. Since there is no objective right or wrong in artistic expression, AI-generated work can be just as valid as human creation.

SaaS companies that are in this sector such as Adobe, Canva or Figma could face a more severe threat than others. As an investor, I’m steering clear from these companies until they can prove their defensive actions are working.

#3: Conclusion

The "SaaSpocalypse" highlights a profound disconnect between Wall Street’s panic and fundamental business reality. While the ~35% sector drawdown assumes AI agents will instantly vaporize "per-seat" software, the double-digit RPO growth of major SaaS players proves enterprise customers aren't leaving.

If anything, this sell-down provides an opportunity for me. Here’s how I plan to position my portfolio:

Buy the “System of Record”: AI is the engine, but proprietary data is the fuel. Companies like MSFT, NOW, SNOW, and FDS provide the mandatory "ground-truth" context AI needs to function. They remain indispensable.

Hold Cybersecurity: The violent sell-off in names like PANW is short-sighted. Given the massive cost of security errors, AI will augment these platforms, but human oversight and deterministic guardrails remain non-negotiable.

Avoid the "Subjective" Danger Zone: Because art lacks an objective "right or wrong," creative SaaS faces genuine disruption from AI generation. I am avoiding this sub-sector until clear defensive moats emerge.

Until my next long-winded post! 🙂

Disclaimer: Word of Caution!

Please DO NOT take this educational post as a buy or sell signal. When it comes to investing, it is important to have your own judgement. Despite my detailed analysis, mistakes may occur, and blindly following could lead you to make similar errors and financial losses. Furthermore, I AM NOT a licensed financial advisor. I’m merely sharing my experiences and opinions only.

Additionally, please note that I hold positions in the discussed stock, and my view may be biased as a result.