Summary

Challenges: The DCF model's accuracy is highly dependent on the quality of input data, making it complex and less reliable.

DCF result: The intrinsic value calculated is either too high or too low when compared with stock price

Preferred method: Relative valuation is still the preferred method due to its simplicity

There are two ways to value a stock. One is to use the Discounted Cash Flows (DCF) Model and another is to use the Relative Valuation approach. The latter has been my go to valuation method. Simply because of 2 reasons:

It is an objective way of valuing a stock

It is quick and simple to use

You can grab a copy of my book here if you would like to learn more about relative valuation method. I explained about it in great detail there.

Conversely, the DCF model involves numerous variables that warrant consideration. Essentially, it's a case of 'garbage in, garbage out,' meaning the model's accuracy is directly influenced by the quality of the input data. This has always been my belief.

However, the primary reason I invest in stocks is to gain returns through dividends or capital gains. These returns are achievable only if the company’s business is able to grow its income and cash flows. That’s why it's undeniable that the valuation of a company is the sum of its future cash flows discounted to present value. This is the big concept of DCF model.

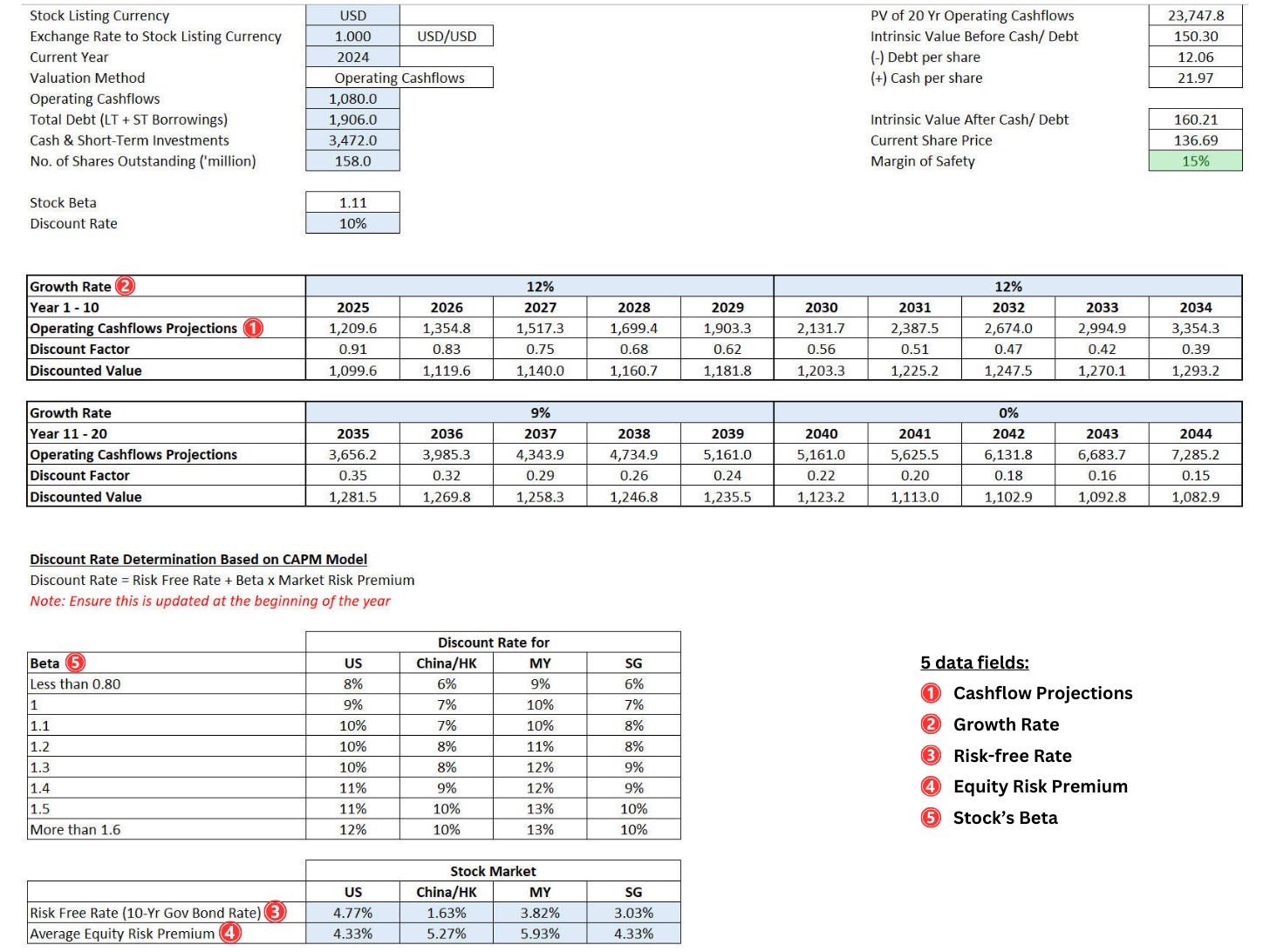

But the challenging part is the integrity of data input into the DCF model. There are 5 data fields requires in below 2 major sections within DCF model:

#1: Cash Flows Projections

As the name suggests, this refers to the company's cash flows. A key decision here is whether to use free cash flows or operating cash flows or net profit after tax.

Ideally, I should use free cash flows because they represent the balance amount a company can distribute as dividends, directly aligning with my investment objective.

However, not many companies can generate increasing free cash flows year over year. Companies in capital-intensive and cyclical sectors often experience volatile free cash flows. For example, those in property development, construction, energy, etc. As such, it is crucial to find companies with stable cash flows for this model to work.

Apart from this, there are 2 more decision points that I have to make.

Number of Years for Projection

How many years should I project the cash flows? Too short, the intrinsic value will be very low. Too far ahead, the intrinsic value will be too high. What is the reasonable number?

I don’t really have an answer here but I have seen many uses 10 years of projection. Some uses 20 years to project the cash flows. I guess ultimately it depends on one’s judgement on whether the business can continue to survive for the next 10, 20 or even 30 years.

But who can tell what will happen exactly in future, not to mention 10 years ahead?

Growth Rates

Choosing the right growth rates for projecting cash flows is crucial for this DCF model. Using high growth rates can inflate intrinsic value, and the reverse is also true. In the past, I relied on the 10-year average CAGR of revenue, net profit, and operating cash flows. However, I find this approach potentially misleading.

Past growth rates do not account for current business challenges that directly impact future growth. Further, companies go through different growth stages at different time period.

For example, a company might have grown at 30% annually 10 years ago when it was small and just starting out. However, a decade later, the same company might not sustain such growth as its business matures.

I still couldn’t find a solution for this part. I can only rely on below external sources:

Guidance provided by Management

Analyst’s estimated growth rates in their reports

Websites such as Finviz, Simply Wall St, Seeking Alpha, etc.

Regardless, there are no such thing as “accurate” growth rates since it involves future outlook. Unless I have a crystal ball that can see the future, I tend to be conservative in determining the growth rates.

#2: Discount Rate

This is used to determine the present value of the projected cash flows. It represents the opportunity cost of capital, considering the risk associated with the investments & time value of money.

In other words, the discount rate reflects the return rate that investors require for an investment, balancing risk and potential reward. Higher discount rate indicates higher risk, resulting in lower present value and vice-versa.

To determine this discount rate, I use the “Capital Asset Pricing Model (CAPM)”. The formula is as follows:

Discount Rate (%) = Risk-Free Rate + (Beta * Equity Risk Premium)

CAPM ensures projected cash flows are appropriately discounted to reflect the risks & potential returns. It provides a systematic approach to determine the discount rate by incorporating the below 3 components:

Risk-Free Rate

This represents the return on an investment with zero risk. Typically, it is the 10-year government bonds’ interest rate or yield. Each country has different government bonds & therefore, different interest rate.

A simple google search would be able to find these figures. However, the challenge is that bond yield changes on daily basis. It is not fixed.

Equity Risk Premium

This is the additional return that investors expect from investing in stocks over the risk-free rate. Again each country has its own average equity risk premium. There’s no way I can reliably determine this figure on my own.

This is where I need to rely on the research of others such as the one in this website: link.

Stock’s Beta

This measures the volatility of a stock relative to the overall market. A higher beta indicates more risk and potentially higher returns, while lower beta indicates less risk. Similarly, there’s no way I can determine this on my own. Normally, I obtain these data from yahoo finance.

Challenges of DCF Model

Looking at all the above 5 data fields (projection years, growth rate, risk-free rate, equity premium rate & stock beta), it is impossible for me to derive the intrinsic value of a stock reliably.

I find myself constantly playing around these 5 data fields, especially the growth rates, whenever I get an intrinsic value that is either too high or too low than its current share price. There’s no way to confirm that the intrinsic value calculated is reasonable. One can only take it as it is.

Hence, the reason why I seldom use DCF model. If you would like to have the DCF Model file, you can download it by clicking here. Remember to download as Microsoft Excel file instead of Google Sheet.

Disclaimer:

The information provided in this blog post is for informational purposes only and should NOT be construed as financial advice. Investing in stocks and ETFs involves risk, and there is no guarantee of profits. Past performance is not indicative of future results. It is important to conduct thorough research or consult with a qualified financial advisor before making any investment decisions. The author is NOT a financial advisor and is sharing his personal experiences and opinions only.